Bad News is Good News: Liberation Day

I think I have had a dozen people a month for the last few years who have told me they are waiting for rates to go down before they will buy a house or refinance. Every grizzled veteran of the industry loves to remind us younger originators how they had no problem doing loans in the double digit interest rate era, and perhaps in 20 years I’ll be telling the next generation how we all managed to handle the jump in interest rates that the industry experienced over the last few years. Combined with the corresponding jump in housing cost, though, it’s been a real challenge for affordability for my clients and I’ve been just as excited as you to have better news to deliver on mortgage pricing.

On the other hand, I know something that you might not: bad news is what will drive mortgage rates down. That’s because ultimately, mortgage rates are established by the demand for that loan by an investor. It doesn’t matter what the internet says or what the guidelines say or what should be happening: at the end of the day your loan happens because someone wants to invest in it. Check out Chapter 1 on Treasury Bonds and Chapter 2 on MBS for some background on how investor behavior drives mortgage prices.

That brings us to the day after “Liberation Day” where the market is reacting to sweeping Tariff announcements and concerns about a global trade war and its impacts on businesses. Investors are looking for safer places to hold their funds after a significant drop to the Dow and strong demand for treasury bonds has pushed the 10 year rate down sharply.

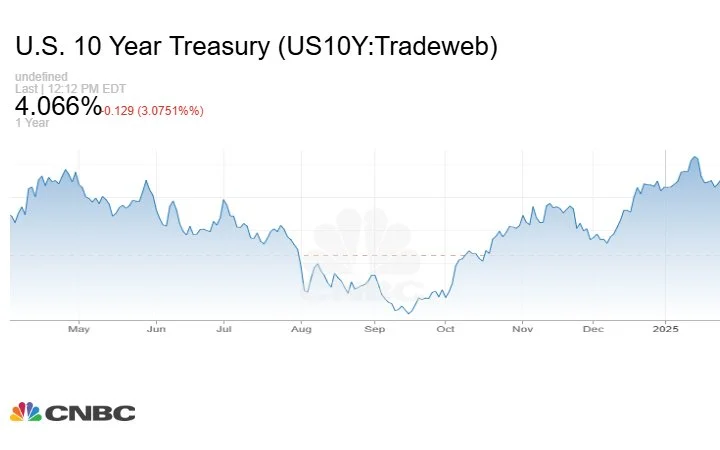

10 year treasury over 1 year

Let’s not get too far ahead of ourselves, though. We are tracking down in a way that gets us back down to last fall, not 2020.

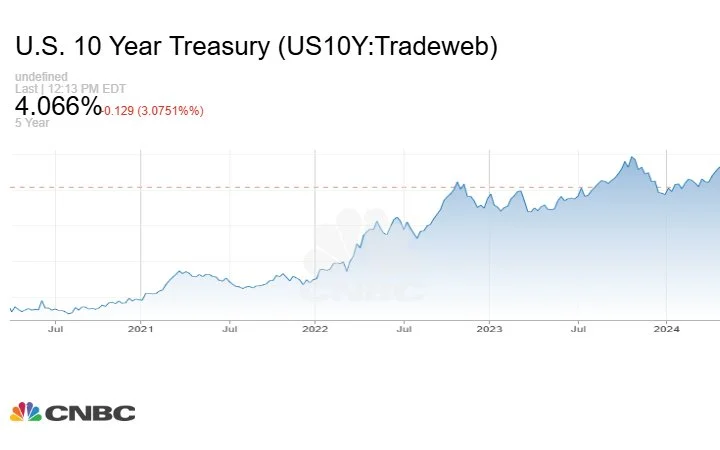

10 year treasury over 5 years

However, when we combine that with strong demand on secondary markets for mortgage backed securities, all signs point to downward movement in interest rates. I tend to side-eye the celebratory posts and articles I see within the industry when mortgage rates go down, since right now, the reason why they’re going down is that massive job cuts have increased unemployment which is a major factor of inflation (more people seeking jobs means lower wages, means lower inflation) and the stock market is showing losses predicting American businesses will face challenges. That’s currently driving investors to safety which means lower rates on your mortgage, but trust and believe that you probably can’t have it both ways where there is a rosy economic outlook AND low mortgage rates.