Why is my rate so high? I have good credit!

Frequently, I am talking to clients about the rate that they qualify for, and they express disappointment or confusion with the rate they are being offered, since they have good credit. Unfortunately, for mortgage pricing, that’s only part of the story. For conventional mortgages, the rate you are offered is determined by a series of pricing adjustments that account for the overall risk according to fannie mae, and only a part of that math has to do with your credit score. That is, unless you are under certain income limits, in which case none of these pricing adjustments apply to you and you will receive the best available rate.

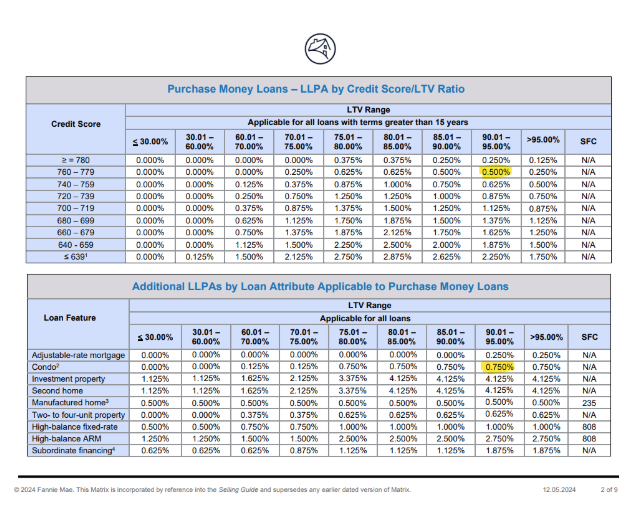

Here is a link to the full document, as of the 12/5/24 revision: Fannie Mae Loan Level Pricing Adjustments

These pricing adjustments are expressed as points, or dollar cost for a given rate, so a 1% in this table means that for a given rate, that feature equals a charge of 1% of the loan amount, and so on.

For our example, let’s assume Peter is over his area’s income limit to have these pricing adjustments waived. He has a 765 credit score and is putting 5% down on a condo as his primary residence. Using these tables, we have a .5% pricing adjustment for the combination of his credit score and down payment, and a .75% pricing adjustment for the property type being a condo

Therefore, Peter will either have to pay 1.25% of the loan amount in cost to have the same rate as someone with a 700 credit score putting down 40% on a single family home (which has 0 risk based pricing adjustments) OR the rate he is offered with no points/cost will be higher to reflect that cost. At the time of writing this article, that was a difference of .5% in rate between my best-priced investor for each scenario!

Fannie Mae Loan Level Pricing Adjustments